Q4 2020, Fintech & APIs

Long overdue for this one.. So, the last couple of months have been quite bumpy in terms of macroeconomic and societal change. A lot of things have happened (a pandemic 🦠 + Kanye West running for president 🗳️) and people are only now getting adjusted to a “new type of normal”.

In the meantime, as an extrovert, I‘ve had more time to consume and read more content 🤓. I have been obsessed with this one thought which Peter Thiel outlined on technological innovation and us living in an era of stagnation. As a quick summary, Thiel outlines that although we think that in the last 40 years a lot of progress has been made (if you measure metrics such as productivity growth and GDP per capita📈), we actually live in an era of stagnation where we always think that we’re on the cusp of a major breakthrough but everything always takes way longer than expected and not much gets done in terms of innovation in major fields of science and technology. Although certainly there‘s been a lot of progress in the fields of information technology, it feels like we have been waiting for AI and autonomous cars for years and all we got was “140 characters on Twitter”, as Thiel likes to put it.

The mental exercise which was outlined and resonated with me was the following:

Imagine yourself in your daily life (ex: on the tube to work, in a room waiting for a doctor’s appointment, in the street having a walk) and now subtract all the screens from the room in which you’re at. Would you notice the difference between now and 1970? The answer is most probably not. Most of the classrooms which kids are in are basically the same as 30 years ago, the way you commute to work is the same (maybe your car is a bit better) and the houses we live in are also the same as not much has changed on an infrastructure side of things.

Where is the opportunity?

Having said the above, I am getting more and more excited by the day as the recent outburst of the pandemic, while tragic and unfortunate on the one hand, also positively accelerated a lot of behaviors and shortened the adoption cycle for many technologies such as contactless payments (no one wants to touch that dirty keypad with their hands!🏧) & many others. All of these combined make us come closer to the next “breakthrough”.

Old Economy → New Economy 🧑🏭

COVID has exposed the fragility of supply chains, especially in the manufacturing industry. U.S. factory output being at an all time low is something that shouldn’t be happening in an era where we proud ourselves to be at the forefront of technology. The trend towards “an automated factory” will get accentuated, with PwC reports showing that 59% of the planned significant investments in Germany’s manufacturing companies will be made in the “use of new technologies & production techniques”.

Whilst I find this exciting, I’m more looking forward to seeing new tools and software enabling workforce productivity to be the more obvious opportunity, given that the chart below reflects the massive acceleration in adoption of e-commerce - but that trend is also reflective of the adoption increase on the manufacturing side & many of other industries that got affected by the pandemic and had to shift gears to maintain productivity 🧑🏻💻. Just like everyone was forced to adopt Zoom, Slack, and other collaboration tools at work, the same is happening in the factory stack for increased productivity.

In E-Commerce, the equivalent of 10 years of adoption happened in just 8 weeks. This leaves clear room/whitespace for a lot of new innovations and enables market maturity for certain business models and innovations to be able to take off! 🚀

If you look at the current situation, especially in the US, the fed is printing money like never before and stimulus checks are being handed out to the population to curb the current situation & with a lot of countries experiencing historic unemployment rates. 🖨️💸

The interesting part of this will be Q4 2020. Especially in the US, in my view, there are going to be 2 hard hits which will spur a cry for innovation, especially for banking & fintech in regards to infrastructure and new services:

- The stimulus checks drying up for most of the population and therefore a shortage of money which will a) squeeze many consumers and b) squeeze small and medium-sized businesses’ which are the backbone of our economies

- The lagged effect of layoffs and the “domino effect” that comes with the economy really getting hit because of the shutdown of the economy in the last months. Let me explain this one more precisely. For big enterprises, layoffs and furloughing take much more time than we think. Just like decisions take longer in hierarchical big organizations, layoffs and firing sprees will also take longer and hit massively in Q4. For big enterprises, just as Elad Gil has put it nicely in his newest blog, the process looks something like this:

- Figuring out the COVID situation (1–3 weeks)

- Figuring out how to get 10,000 employees to work from home and become somewhat productive (4–5 weeks)

- Figure out the impact of the economic slowdown to the business and the customers (2-4 weeks)

- Decide how to cut costs and pull together layoff plan (4 weeks)

- Take action with layoffs, IT buying freeze etc. (4–8 weeks)

Add these together, and you have a process of about 4–8 months to plan and execute all of these steps, with layoffs being the last one. Given that we are only a couple of months into COVID, much of the damage is yet to come (Q4).

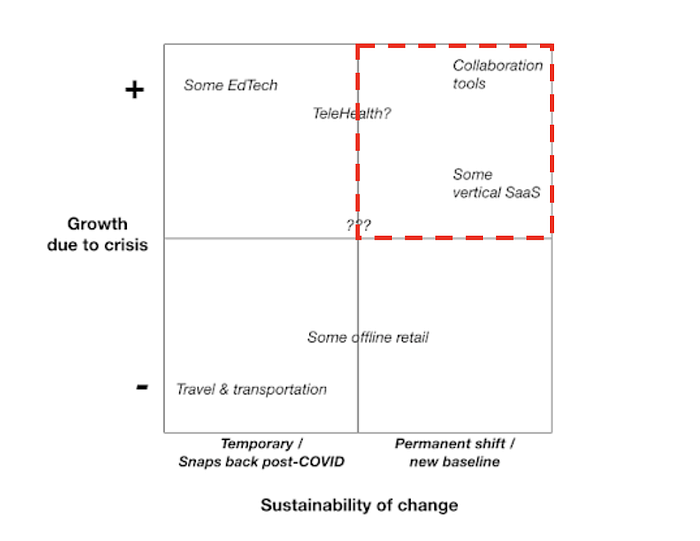

If you look at the upper matrix, that is a good way to segment startups and if the “growth due to COVID” will be sustained or not. Focusing on the upper right corner (in red), that’s where I think many new fintech startups can position themselves.

More specifically, this is where in my opinion, whitespace for vertical innovation has been created. In comparison to horizontal innovation, which are companies that are essentially built around emulating successful ideas in a different geographical location (challenger banks are now everywhere with multiple geographies having different players), vertical innovation has the potential to create meaningful shifts in the long run.

I’ve been seeing companies in different verticals of fintech trying to solve a wide range of issues:

1) The unbundling of financial institutions (banks)🏦

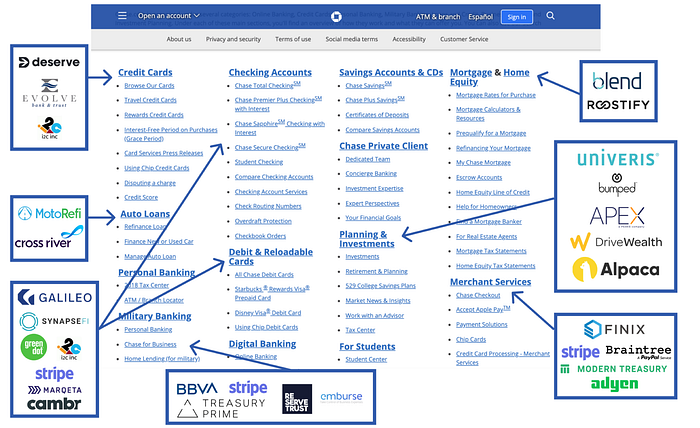

Financial companies historically were large fossilized 🦖 applications that served the entire suite of financial products to all of their customers. For example, Chase Bank in the U.S. provides all of these services across these segments:

- Consumer — Checking accounts, savings accounts, debit cards, credit cards, FX, remittance, and payments.

- SMB — Business checking and savings, debit and credit cards, business lines of credit, loans, merchant services, credit card processing, and PoS systems.

- Enterprise — Commercial checking, financing, real estate, employee benefits, institutional investment, investment banking, securities, and treasury management.

As fintech startups are gaining traction, they largely target narrow verticals and customer segments. Below is an overview of all the infrastructure startups showing how each fintech company is attacking a very specific product segment that Chase Bank provides:

Fintech infrastructure startups have had some really good momentum in the last months, with Solaris Bank raising $67.5 million at a $360 million dollar valuation, Galileo raised $77m, SynapseFi raised a $33m Series B among many others. As these grow, more and more verticals of the financial infrastructure will be tackled and disrupted, which will force the incumbents to have to innovate. 💡

2) Financial Wellness (enabled by APIs) 💆♂️

As mentioned above, stimulus checks will be drying up in the later quarters of the year and the question will arise whether the unemployment and the macroeconomic situation will get better. A lot of data points towards that not happening (the hunch above which mentioned that the firing wave will come in times of Q4), + people inevitably getting squeezed on the financial side, causing even more financial “stress” for consumers and businesses. The most staggering data point to me, which relates to retention, which by the way is one of the biggest problems that high-growth startups are experiencing nowadays in the fierce fight to maintain top-employees:

80% of employees would switch to a company that cares more about their financial well-being. (Source)

Startups such as Trezeo, allow gig-workers who don’t have all the regular benefits of an employee such as a regular guaranteed income, holiday pay, insurance, and health care to have a “safety-net” and not feel “short on cash”.

Others include Origin, a startup that offers employees in companies a “Financial Advisor-as-a-Service model”. Considering that employees spend an estimated two to four hours each week dealing with their personal finances, an offering like Origin’s seems like a no-brainer for employers looking to both improve employee productivity and employee retention.

The only thing holding back such offerings (Origin f.e.) earlier in time were the kind of open banking APIs that exist today.

3) (Challenger)-Banks will allow credit card issuing via APIs 💳

In the last years, we have seen the rise of challenger banks such as Chime (U.S.) and N26 and Monzo (Europe) launching debit cards and new “deposit accounts”. These are enabled by APIs that exist for launching deposit products, such as Galileo (U.S.) and Solaris Bank (Europe). Its APIs have fueled functions including direct deposit, account setup, funding, and check balance, among other features. Galileo and Solaris’ clients include Chime, Monzo, KOHO, Revolut, Robinhood, TransferWise, and Varo.

But still, there are hardly any APIs that exist for banks to launch credit cards and this will very likely change in the next couple of months (Q4 😜).

Additionally, my hunch is that there’s going to be more private-labeled credit card offerings, focusing on different verticals and use-cases. Fintech credit is still early, but startups such as Tymit, which allow consumers and businesses to make all purchases in installments across 3–24 months, which is a brand new concept in the space.

APIs will be the suppliers in a “software based economy” and will increase the speed of building new and better businesses 🚚 🤖

This also ties into the other trend which is..

4) Verticalized banking and embedded fintech will continue to grow🚦

Given that the financial infrastructure will be unbundled and the capacity of launching financial products and services has and will be made cheaper/easier, this will allow for startups to emerge that will cover the space of verticalized banking. What does this mean?

The growth of: “banking for *INSERT DEMOGRAPHIC*”.

The tweet below summarizes these “1% of the population” markets:

Some of these already have products that exist for their particular segments (military & education) but it shows how many people are in each segment and how big a product that serves just 1% of the population can be.

Having said the above, there is also a clear trend towards “embedded fintech”.

Rather than standalone applications, financial features are also being merged into all of the business applications that people are using already. Here are several examples:

- Uber — Launching Uber money to allow drivers to collect earnings in real-time & issue credit/debit cards to spend their balance.

- Grab — Created their own digital wallet to be able to hold and spend value in their digital wallet (similar to WeChat pay).

- Google — Now offering checking accounts through Citigroup and Stanford Federal Credit Union.

- Facebook — Is trying to launch Libra, one of the more ambitious bets to develop its own digital currency.

- WeChat — Has 1 billion users and does $1 billion in total daily payment transaction volume via WeChat Pay.

5) ARR Securitization💰

Very much inspired by John Luttig’s new post, the concept of getting your annual recurring revenue subscriptions’ cash now, to grow even faster - is something that incumbent banks aren’t even thinking about in their dreams, but it is very much becoming a reality. 💤

Getting up to the full annual value of your booked monthly and quarterly subscriptions and scaling your business without dilution or debt makes a lot of sense, especially with the concept already working for some later-stage companies. If you want to dive into more detail, this article goes into the more granular forms of what this ARR securitization can look like.

Companies like Pipe and Clearbanc are already starting to destigmatize securitization, and it will only become more culturally normalized in the coming years. The crux of the matter for companies targetting smaller businesses with less than <50k MRR will be the validity of data (since small companies report on different data) & given that 90% of new startups will fail, figuring out how to target that remaining 10% through a good enough risk framework (here’s where the magic lies 🔮).

Thanks for reading and I hope this article shed some light on the shifts and trends in Fintech, APIs & Q4 2020! Also, open for comments and different views regarding the topic 🤗